Iran War Sends Markets Off Course

Redacción Mapfre

RoadMap: Monthly market report prepared by the Mapfre AM team

What happened over the past month?

The picture painted by financial markets over the past month varies greatly depending on where the period is considered to end. As of Friday, February 27 (the last trading day of the month), European equities had risen more than 3%, emerging markets over 5%, while U.S. indices ended the period flat—or negative in the case of the Nasdaq. Meanwhile, yields on government bonds declined, particularly at the long end of the curve, leading to a flattening of yield curves. Within fixed income, corporate bonds fared the worst, with credit spreads widening, especially among issuers with lower credit quality. On Saturday, February 28, the United States and Israel launched a military offensive against Iran, triggering turbulence in the markets in the early days of March.

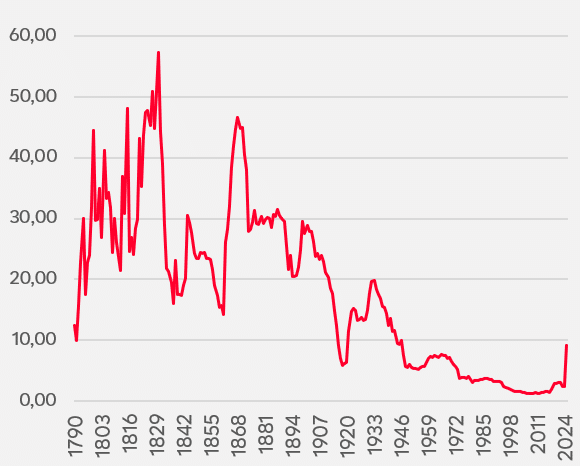

Before tensions escalated in the Middle East, markets had been focused on the U.S. Supreme Court’s decision that the International Emergency Economic Powers Act could not be used to justify the tariffs announced in April 2025, as well as on the disruptive impact of artificial intelligence (AI) on a number of companies. Beyond the elimination of these tariffs—which could ultimately bring the effective tariff rate to around 10%, according to estimates by Yale University—the court’s ruling also weakens Donald Trump’s political leverage. Under the decision, he would only have a 150-day extension to keep the tariffs in place, after which Congress would need to approve them. Refunding the duties collected so far could take months, and although this may generate some short-term uncertainty, tariff decisions are unlikely to be as abrupt as they have been to date.

Figure 1: Effective tariff rate (Yale Budget Lab)

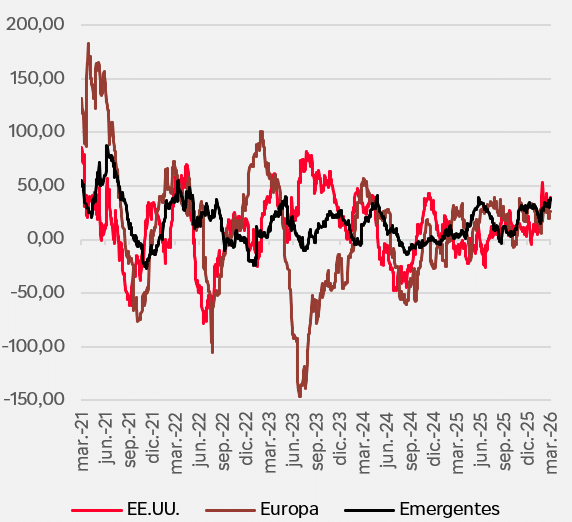

As for AI, the market has continued to penalize companies most likely to be negatively affected. Sharp stock market declines in companies such as Adobe, Microsoft, and IBM are part of the rotation within equity markets, which had been favoring sectors more closely linked to the “old economy” (given their lower exposure to disruption) and with a more cyclical profile. This shift also reflects the positive macroeconomic data released during the month: business confidence indicators pointed to a continuation of the previous year’s economic cycle (our baseline scenario for this year) and a cooling of inflationary pressures.

Figure 2: Macro surprises index

Uncertainty surrounding the new technology has also spread to corporate bond markets. Major companies linked to AI have increasingly relied on debt markets to finance their capital investments, meaning that any doubts about their future economic profitability put pressure on the price of these bonds. In addition, much of this financing has taken place through private debt markets, which are now coming under scrutiny after several companies defaulted and some funds were forced to temporarily suspend redemptions.

All of this was overshadowed on the final day of the month by the outbreak of war in Iran, which has since spread to other Gulf countries following Iran’s response to the attacks. At this stage, it is very difficult to predict the final outcome. However, markets will be watching closely the conflict’s impact on energy prices, as these are the key transmission channel to the global macroeconomy and, ultimately, to asset prices.

What's our take?

The escalation of military tensions across the Middle East following U.S. and Israeli attacks on Iran has not, for the time being, altered our constructive outlook for growth in 2026. However, it does move us closer to our alternative scenario, in which the accumulation of “frictions” leads to downside risks for growth and upward pressure on inflation.

Energy is the main transmission channel. Roughly 20 million barrels of oil pass through the Strait of Hormuz each day, along with around 20% of global liquefied natural gas, with Qatar serving as a key supplier to Europe and Asia. Alternative capacity is limited. As a result, a closure of the strait, partial disruptions, or systemic damage to the production capacity of countries in the region would drive up energy prices and increase the risk premium across asset classes.

The macroeconomic impact will depend on the duration of the conflict, how the Strait of Hormuz is managed, and any potential damage to the region’s oil and gas infrastructure. Financial markets tend to absorb short-lived shocks better than structural ones. A more prolonged conflict with regional spillovers would therefore significantly amplify the impact. Higher inflation in energy products, logistics costs, and industrial inputs would weigh more heavily on net-importing economies such as Europe and Asia. From a growth perspective, higher energy prices would erode private consumption, while rising uncertainty would likely curb investment.

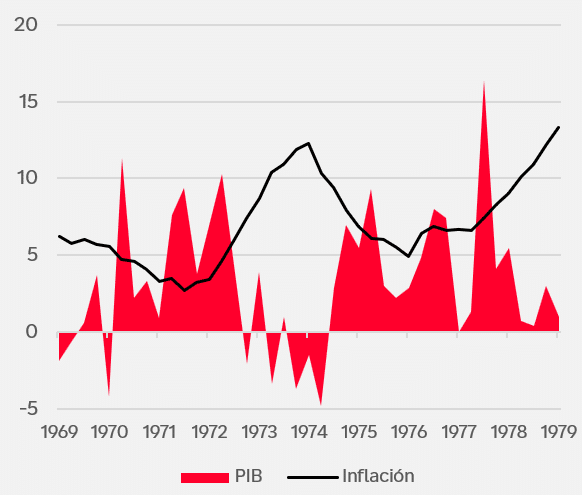

That said, even in the worst-case scenario, we do not believe we are facing a crisis comparable to the one in the 1970s, triggered by the OPEC oil embargo and the 1979 Iranian Revolution.

Figure 3: U.S. GDP and inflation during the 1970s

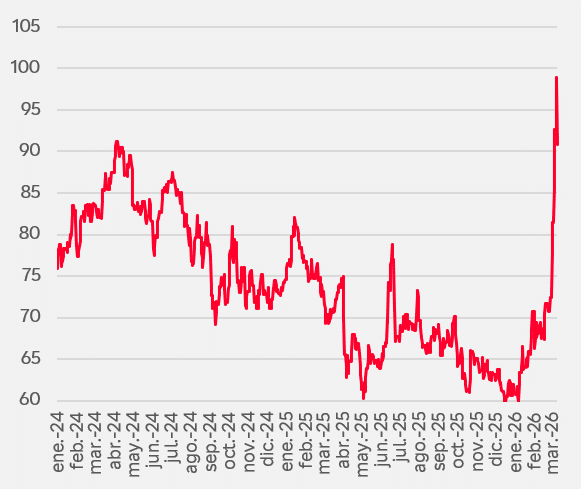

At that time, the situation was very different: the global economy was moving away from the gold standard, the United States was not energy independent as it is today, and economies were far more dependent on oil than they are now. If we are to draw any meaningful parallels, the only practical approach is to closely monitor three key factors—duration of the conflict, developments in the Strait of Hormuz, and potential structural damage—to adjust portfolios in what will likely remain a fluid environment. Markets will be watching the price of oil especially closely. A sustained price above 100 dollars per barrel would significantly escalate the scale of the conflict’s economic repercussions.

Figure 4: Oil price

With geopolitical risk elevated and uncertainty surging, it is only natural that market sentiment has deteriorated significantly compared with the start of the year. However, if we look at the largest destruction of market value so far this year, it has not been driven by geopolitical factors but rather by the disruptive impact of AI on companies whose competitive advantages appear to be vanishing almost overnight—particularly in the software sector. Other service-related sectors, such as financial services and real estate, have also been affected. As a result, equity indexes remained close to their highs prior to the hostilities in the Middle East, but with significant dispersion in returns within the indices themselves.

All of this comes as the earnings season for the final quarter of 2025 draws to a close, a period in which the sources of earnings growth have also shifted. According to estimates by Deutsche Bank, the 10 largest companies in the S&P 500 have accounted for roughly two-thirds of the index’s earnings growth since 2022. In the most recent quarter, however, earnings growth has broadened beyond the largest companies, with eight of the eleven sectors posting positive contributions and half of all companies reporting growth of more than 10%. The fact that Nvidia fell 5% after reporting outstanding results suggests that expectations—and positioning—may have become too elevated.

Beyond the sector rotation mentioned earlier, European and emerging-market equities had led gains so far this year, supported by favorable macroeconomic prospects, a growing need to diversify positions away from the United States, and expectations of a weaker dollar. The war in Iran has reversed this trend, as both Europe and Asia are likely to be among the regions most affected if the conflict drags on or its economic impact intensifies.

At a time when risk appetite is declining, it is understandable that investors have reduced exposure to positions that had generated the strongest gains. Moreover, if geopolitical tensions persist, European and emerging-market equities may face additional pressure, suggesting that a more neutral stance toward equities is now warranted.

The new environment created by the war in Iran has also made fixed income more attractive from two perspectives. On the one hand, weaker market sentiment is prompting many investors to shift toward safe-haven assets such as government bonds, which currently appear more attractive from a valuation standpoint than alternatives such as gold or other reserve currencies. On the other hand, while the recent increase in oil prices and the potential for inflationary pressures pose an obstacle to stronger conviction, at current levels, this is a risk we are willing to take on a tactical basis.

As for corporate fixed income, our view remains unchanged. We continue to see value at current levels, and any widening of corporate spreads would be viewed as a buying opportunity, as we do not expect the conflict to last long enough to materially alter credit fundamentals.

What are we doing?

The current environment calls for greater caution given the uncertainty surrounding the conflict in Iran. As a result, we have decided to tactically neutralize our overweight in equities in case the more adverse scenarios outlined in our Market Flash Note begin to be priced in with higher probability. We have been reducing our equity exposure by taking profits in Europe and Asia, which had outperformed U.S. equities and are also regions that would likely suffer more from the consequences of a prolonged war. In fixed income, the rise in interest rates so far in March is bringing yields closer to levels where, with considerable caution, we would consider increasing duration. We have not made any changes to corporate bonds. These adjustments have been tactical in nature, as we continue to maintain a positive outlook for the rest of the year.

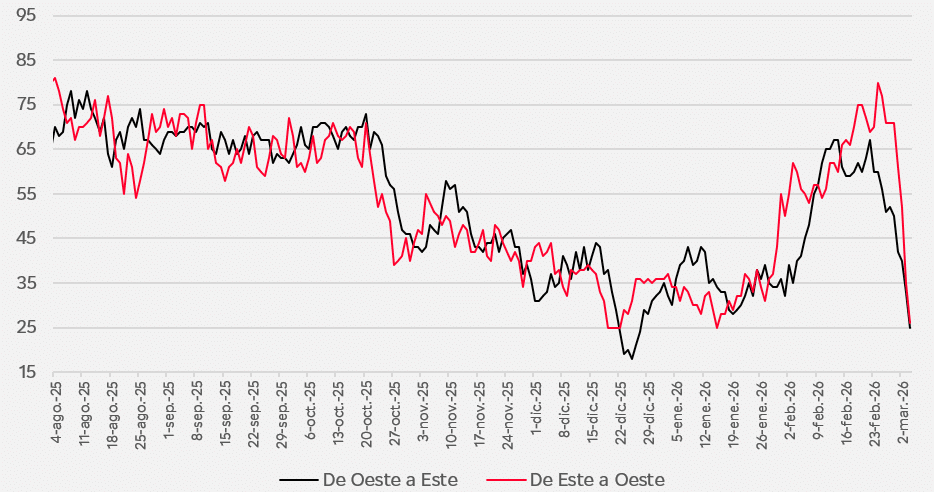

Chart of the month

The Strait of Hormuz

- How the Strait of Hormuz is managed will be key to assessing the potential impact on the global macroeconomy and asset prices.

- An increase in oil prices acts like a tax that drains households’ purchasing power and weighs on growth. For this reason, it is important to monitor the number of oil tankers passing through the strait, given that around 20% of the world’s oil consumption flows through this route.

- According to data from the past week, the number of ships traveling eastbound (presumably loaded with oil) and those traveling westbound (presumably returning to load oil) has dropped sharply, despite the United States’ willingness to provide both military and financial protection for these vessels.

Estimated number of oil tankers passing through the Strait of Hormuz

Source: Bloomberg

Own elaboration