The seeming paradox of the ECB

Redacción Mapfre

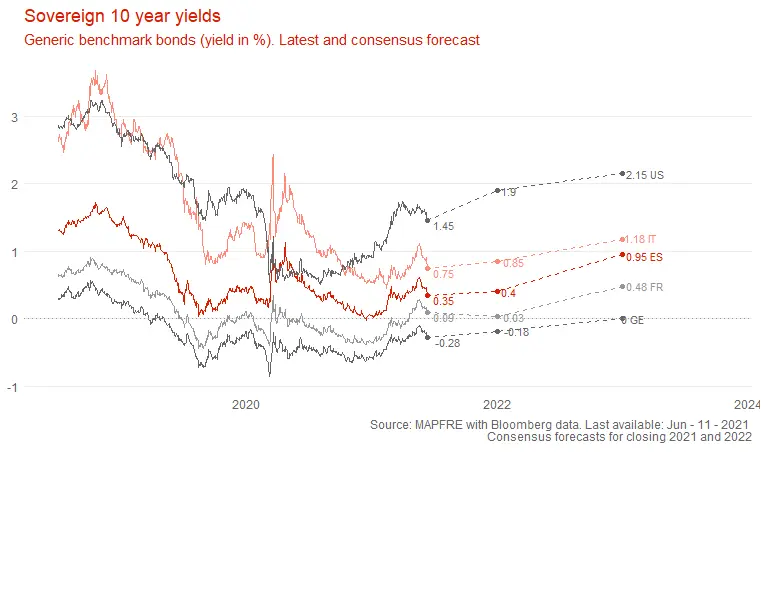

Desperately seeking financial stability

The higher the inflation in the US, the more dovish the ECB's policy should be. This apparent paradox arises from trying to explain how the European monetary authority works in light of its meeting of June 10th. It surprised with a much more bearish tone than investors expected, but two things became clear. First, the main variable the ECB follows is core inflation, and it is going to remain very low for many years to come. They are therefore convinced, as many analysts are, that current developments are merely temporary. Second, and much more importantly, this frees their hands to pursue the Bank's other (now primary) objective: financial stability.

The real goal is to keep curves as lowest as possible

In practice, and after what has happened in recent years, we have come to identify financial stability with preventing rises in sovereign curves. In theory, this should not be the case. A healthy market allows prices to fluctuate freely. However, in the current context, such a rise would threaten the public balances of the EU governments, at a time when an expansionary fiscal policy seems necessary, and has to be paid for.

Moreover, flooding the system with euros indirectly devalues the debt; it reduces it in real terms. Contrary to popular belief, debt devaluation is not caused by CPI inflation but by monetary debasement, especially when the same institution that prints money increasingly holds such debt. At the same time, facilitating such spending and avoiding alarmist headlines helps to consolidate moderate governments in Europe to the detriment of Eurosceptic ones, which would also threaten such stability. The case of Italy is paradigmatic.

On the other hand, an eventual sustained rise in the curves also threatens the capital position of European banks. This has proved to be one of the weakest links in the system (paradoxically, the rise would allow them to return to their traditional business, but this seems to matter less to the ECB). Any threat to this capital position is a direct risk to the aforementioned financial stability. Hence, the situation in which the monetary authority and the commercial banks themselves seem trapped.

In turn, keeping the curves low helps to moderate the value of the euro. The dollar has depreciated sharply because its central bank insists on massive currency printing, even in the presence of high CPIs. Normally, as the year progresses, this situation will change and the dollar will appreciate, to the detriment of the euro. But in the meantime, the euro is possibly higher than the ECB would like. Therefore, insisting that euros are going to be printed in large quantities for much longer helps to put downward pressure on the European currency, thus apparently facilitating the European recovery.

The paradox is just an implementation of such undeclared policy

In short, as long as there is no certainty of very sharp rises in European core inflation, the ECB's main objective is to keep rates curves low against all odds. When US inflation rises sharply, there is an upward drag on European curves which, if the above is true, the ECB is forced to compensate by reaffirming its commitment to stimulus, and even increasing it. This is obviously a very dangerous exercise, since it implies continuing to hold market prices in the face of increasingly powerful opposing forces. But it is achievable, insofar as the ECB's purchase volume is sufficient to absorb more than the net issuance of Eurozone governments this year. It is also a bet that European core inflation will not rise and/or US core inflation will fall again. Maybe they are wrong, maybe not, but they have enough room to keep the bet for many months to come.

Alberto Matellán, Chief Economist at MAPFRE Inversión