US trade policy enters a new, less explosive but more uncertain phase

Redacción Mapfre

Eduardo García Castro, expert economist at Mapfre Economics

The suspension of the tariffs imposed by President Donald Trump under emergency powers marks a turning point in U.S. trade policy. The Supreme Court’s decision not only brings an exceptional period to a close—one in which the White House extended tariffs to virtually all of its trading partners—but also requires a reassessment of the legal framework that will underpin tariff strategy in the months ahead. The implications extend beyond the legal dimension, encompassing the broader climate of regulatory uncertainty, the reconfiguration of corporate and investor incentives, and the potential redirection of trade flows going forward.

Although markets appear to have received the ruling with relative calm, the decision ushers in a new phase in which Washington must rebuild its trade policy gradually—preserving fiscal revenues, reshaping bilateral agreements, and recalibrating its political message to an electorate particularly sensitive to prices and employment.

The first move: a global “emergency” tariff under a new legal framework

Unable to continue relying on the previous emergency authority, the Trump administration has turned to an alternative legal mechanism that allows for temporary, broadly applied tariffs. The response was swift: a 15% tariff on virtually all imports, designed to remain in place for 150 days. This measure serves as a bridge toward a new regulatory framework that has yet to be defined. The main advantage is speed, as it can be implemented without a lengthy consultation process. The drawback is that it does not provide the negotiating flexibility previously afforded by emergency powers. By design, the instrument is rigid: it applies across the board, does not differentiate by country, and cannot serve as bilateral leverage to secure concessions.

The immediate effect is a moderate decline in the average effective tariff rate, particularly for countries that had previously faced duties above 20%. China stands out among the main beneficiaries, as part of the additional surcharges accumulated in recent months has been eased, providing meaningful relief for its exporters. Several emerging Asian economies—including Bangladesh, Vietnam, and Indonesia—as well as some Latin American providers also see a noticeable improvement in their relative position. By contrast, advanced partners that had already secured favorable terms, such as the European Union, see little change in their effective tariff rate. In relative terms, this reduces the advantage achieved under the previous framework. At the same time, countries such as the United Kingdom and Australia face a relative increase compared with the prior arrangement, leaving them temporarily in a less favorable position (see Table 1).

Overall, the aggregate macroeconomic impact is limited, and current estimates point to only marginal effects on U.S. and global GDP and inflation this year. However, a closer look reveals a far more complex and heterogeneous picture at the sectoral level—dynamics that are largely obscured in the broader macroeconomic reading.

Winners and losers: a quiet reshuffling of the tariff landscape

Although temporary, the new framework introduces a clear redistribution of tariff burdens. Economies that had previously faced extraordinary duties for reasons not strictly related to trade record the most significant relative gains. These include several large manufacturing exporters, as well as certain Asian economies linked to textiles, consumer goods, and mid-range electronics.

At the opposite end of the spectrum, several advanced partners that had secured tariff reductions through bilateral agreements now find themselves in a comparatively less favorable position. This is not due to a substantial increase in their own tariff levels, but rather to the sharper decline observed in other countries, eroding the relative advantage achieved during the previous cycle of accelerated agreements.

Table 1

| Geography | Base scenario in february | Global 15% tariff under Sec. 122 | Var p.p |

| World | 13,5 | 11,9 | 1,6 |

| Brasil | 17,9 | 9,6 | 8,3 |

| China | 35,2 | 27,2 | 8 |

| Bangladés | 34,9 | 30 | 4,9 |

| Pakistán | 27,7 | 23,9 | 3,8 |

| Sudáfrica | 11,3 | 8,1 | 3,2 |

| Camboya | 25,4 | 22,8 | 2,6 |

| Indonesia | 22,1 | 19,7 | 2,4 |

| Vietnam | 17,3 | 15,3 | 2 |

| India | 14,9 | 13,6 | 1,3 |

| Tailandia | 14,7 | 13,5 | 1,2 |

| Filipinas | 12,3 | 11,2 | 1,1 |

| Canadá | 6,3 | 5,3 | 1 |

| Malasia | 10,7 | 9,7 | 1 |

| México | 9 | 8,7 | 0,3 |

| Bélgica | 5,2 | 5,2 | 0 |

| Croacia | 9,5 | 9,5 | 0 |

| Rep. Checa | 12,1 | 12,1 | 0 |

| Dinamarca | 12,3 | 12,3 | 0 |

| Ecuador | 5 | 5 | 0 |

| Estonia | 15,2 | 15,2 | 0 |

| Finlandia | 11,4 | 11,4 | 0 |

| Francia | 11,5 | 11,5 | 0 |

| Alemania | 12,7 | 12,7 | 0 |

| Grecia | 11,1 | 11,1 | 0 |

| Hungría | 8,5 | 8,5 | 0 |

| Irlanda | 2,5 | 2,5 | 0 |

| Israel | 10 | 10 | 0 |

| Italia | 13,3 | 13,3 | 0 |

| Japón | 11,6 | 11,6 | 0 |

| Letonia | 12,4 | 12,4 | 0 |

| Lituania | 10,9 | 10,9 | 0 |

| Luxemburgo | 19,8 | 19,8 | 0 |

| Malta | 5,4 | 5,4 | 0 |

| Países Bajos | 6,9 | 6,9 | 0 |

| Polonia | 12,4 | 12,4 | 0 |

| Portugal | 8,5 | 8,5 | 0 |

| Rumanía | 16,1 | 16,1 | 0 |

| Eslovaquia | 14,8 | 14,8 | 0 |

| Corea del Sur | 12,9 | 12,9 | 0 |

| Eslovenia | 2,9 | 2,9 | 0 |

| España | 12,2 | 12,2 | 0 |

| Suecia | 12,6 | 12,6 | 0 |

| Suiza | 6,5 | 6,5 | 0 |

| Taiwán | 7,4 | 7,4 | 0 |

| Turquía | 18,4 | 18,4 | 0 |

| Colombia | 4,7 | 5,8 | -1,1 |

| Reino Unido | 7,9 | 9,3 | -1,4 |

| Perú | 5,1 | 6,6 | -1,5 |

| Australia | 6 | 7,6 | -1,6 |

| Chile | 4,2 | 5,9 | -1,7 |

| Costa Rica | 6,8 | 9,6 | -2,8 |

Fuente: Mapfre Economics

That said, it would be premature to anticipate a significant reconfiguration of supply chains. While the current differentials are politically significant, they do not appear sufficiently persistent or deep to trigger large-scale relocations. Trade flows are therefore expected to continue prioritizing factors such as geographic proximity, logistics infrastructure, sectoral specialization, and above all, regulatory predictability.

The key question: the second half of the year

The temporary global tariff expires in just five months, and the Trump administration has already indicated that, after that period, it will activate more durable mechanisms based on formal investigations into trade practices and national security risks. These instruments—slower but legally more robust—will allow for the selective targeting of specific sectors and countries, implying that the tariff landscape is likely to shift again.

This outlook creates a scenario in which tariff volatility may increase. Once the temporary framework expires, differentiated duties could come into effect, aimed at strategic sectors such as semiconductors, critical minerals, pharmaceuticals, steel, industrial components, and sensitive technology goods. In other words, the new global tariff represents an initial phase of adjustment rather than the final stage of the process.

The fiscal issue: revenue, litigation, and the deficit factor

The Supreme Court’s ruling also reopens the debate over the potential reimbursement of tariff revenues collected under the now-invalidated authority. The amounts involved are substantial: potentially more than 150.0 billion dollars in accumulated revenue. Although the government has indicated that it does not anticipate immediate refunds and that litigation could extend for years, the mere possibility introduces a degree of fiscal uncertainty. Even so, the official expectation is that tariff revenues in 2026 will remain largely intact, with any future reimbursements offset by new revenues generated through alternative instruments to be implemented from the summer onward.

Financial markets appear to interpret the development as one of fiscal continuity. The yield curve has shown a slight steepening bias, spreads have moved moderately, and there have been no signs of liquidity stress. Even under a more adverse scenario involving accelerated reimbursements, the substantial cash balance held by the U.S. Treasury would likely provide a sufficient buffer to avoid short-term pressure on debt issuance.

Inflation, consumption, and monetary policy: limited impact

The overall assessment is that the tariff shift does little to alter the projected macroeconomic path. Any disinflationary effects are likely to be marginal and insufficient to change the timing of interest rate cuts already anticipated by both the market and the Federal Reserve.

Nor does the rollback of previous tariffs appear likely to materially shift the trajectory of consumption. Although household savings rates remain low and there are signs of fatigue in durable goods spending, demand for services continues to hold up. Business investment—supported by automation and technology—also continues to provide some underlying support.

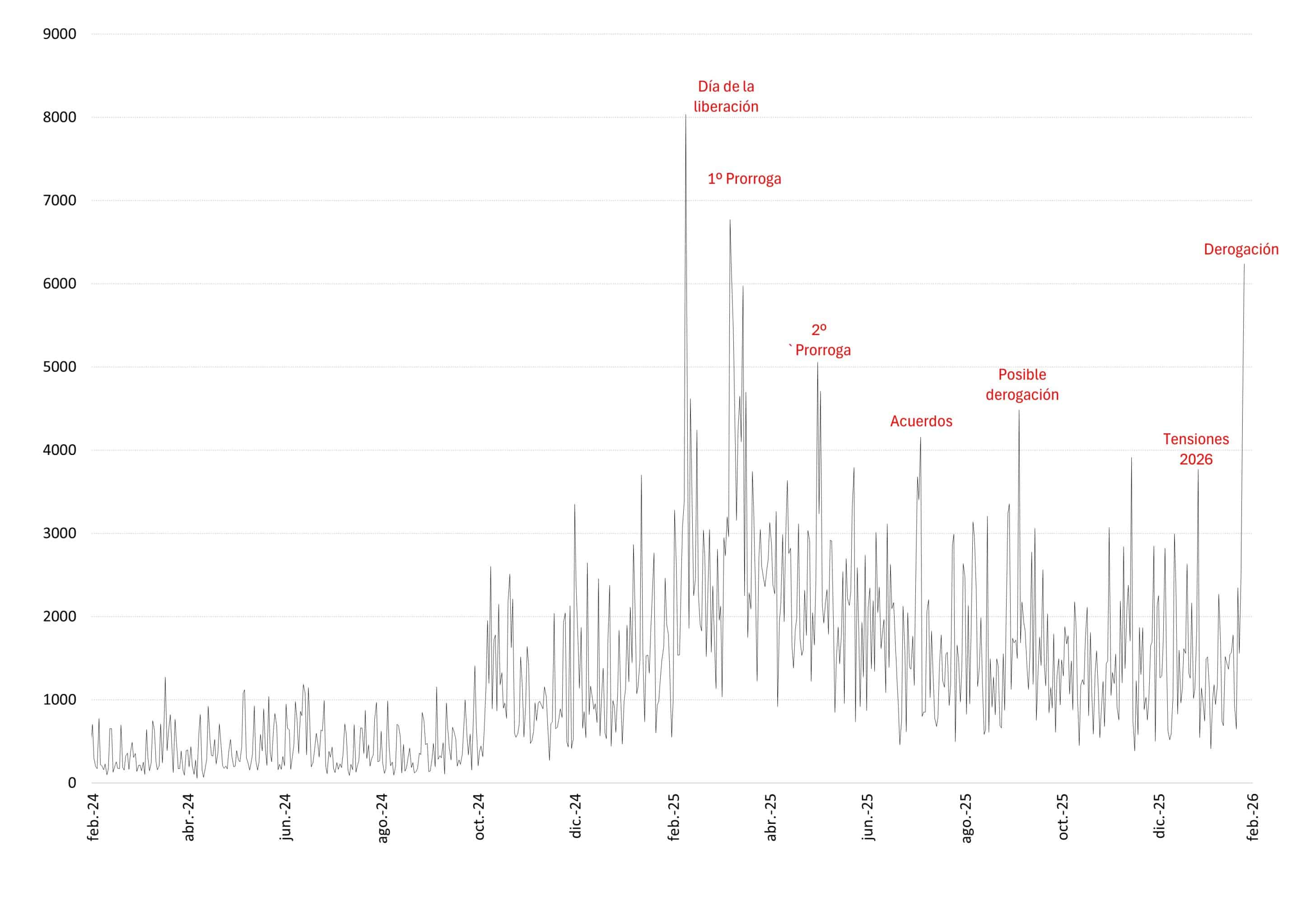

The psychological variable: rising uncertainty around trade policy

The Supreme Court’s ruling also challenges the view that had taken hold in recent quarters—that U.S. tariff policy had entered a phase of relative stability (see Chart 1).

Chart 1: trade policy uncertainty

Source: Mapfre Economics (con datos de EPU)

The loss of such a flexible instrument means the U.S. government will now have to rely on more bureaucratic, slower-moving mechanisms, with greater involvement from regulatory bodies. This introduces a dual dynamic:

- Lower risk of abrupt escalations. Large tariff increases can no longer be imposed overnight.

- Greater cumulative uncertainty. If future tariffs depend on formal investigations, public hearings, and review processes, the regulatory horizon becomes less clear for exporters and investors.

The likely outcome is an environment of ongoing vigilance, in which neither a severe deterioration can be ruled out nor expectations firmly anchored to continued stability. As a result, further episodes of front-loading and anticipatory import activity may reappear over the course of the year, as seen in recent periods.

Trade relations and bilateral agreements: scope for renewed negotiation

The Supreme Court’s decision also casts uncertainty over bilateral agreements previously reached between the United States and its trading partners. While most sector-specific restrictions tied to national security are expected to remain in place, tariff reductions that depended on the now-invalidated mechanism could lapse once the transitional phase ends. This creates the possibility that some trading partners may revisit prior commitments, particularly if they view the original negotiations as having been based on a legal framework that no longer applies. At the same time, the Trump administration may be tempted to use the new instruments as leverage to rebalance ongoing negotiations, including those involving India, certain European economies, and China.

Conclusion: a new phase, less explosive but more uncertain

In sum, the Supreme Court’s ruling does not abruptly alter the near-term macroeconomic trajectory, but it does reshape the foundations on which U.S. trade policy will be built in the months ahead. Growth, inflation, and financial conditions show little immediate disruption. However, it would be a mistake to interpret this surface stability as evidence of lasting normalization. What is emerging instead is a tariff regime that is less prone to sudden escalation but increasingly uncertain—more complex, less predictable, and potentially more consequential for specific sectors and trading partners.

The real impact, therefore, lies not in the short term, but in the institutional framework the United States is now rebuilding, and in how its global counterparts respond in an environment where legal stability can no longer be taken for granted.