More uncertainty: Covid worsens the scenario for China’s economy

Redacción Mapfre

What do tycoons like Elon Musk, Bill Gates, Mark Zuckerberg, and Tim Cook have in common? All of them, besides being the visible heads of their respective companies, are clear examples that the United States continues to maintain its global supremacy. Alongside these famous names, the position of the U.S. economy has been reaffirmed these days with the dollar as the protagonist, recovering its presence with respect to the euro—which has fallen, for the first time in five years, below the $1.07 range.

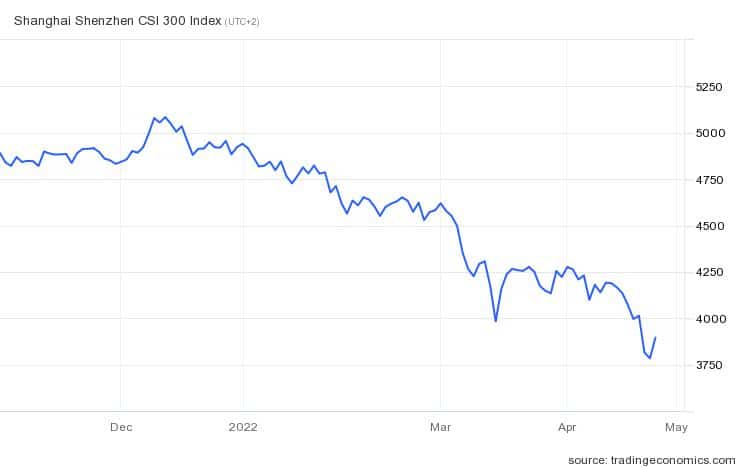

The question, however, takes a 180-degree turn when the analysis shifts to more than 11,000 kilometers away. On the other side of the Pacific, China, which had been pointed to as a future global economic leader (and, for the time being, maintains that status), finds itself in Covid-stricken limbo: stringent measures to mitigate the new wave of infection in the Asian giant have added to the country’s uncertainty. In the wake of the restrictions, which have resulted in greater discontent among the Chinese population, the situation in supply chains—which were already weighed down by disruptions in raw materials—has increased pressure on its activity, heightening fears of an eventual economic recession in the country (in fact, its latest PMI data for industry and services contracted—48.8 points vs 51.2 in February). “Its situation is far from positive, and some analysts are already significantly revising their forecasts downward,” asserted Ismael García Puente, investment and fund sector manager at MAPFRE Gestión Patrimonial (MGP).

For his part, Gonzalo de Cadenas-Santiago, executive director of MAPFRE Economics, added to the equation the problems associated with the real estate market that continue to weigh down the region: “We must not forget the ‘Evergrande case’ and the sovereign-financial crisis they are facing.” García Puente recognized, however, that, in the face of these events, “it is difficult to draw conclusions, and even more so with the VIX (market volatility reference index) close to 30 points.” But experts consider this to be bad news for its internal dynamics and the gears of the world economy.

Europe is not risk-free either

Readjustments in growth estimates and inflation globally (both aggravated by the situation in Ukraine and China, mainly) are making “the market picture more difficult to make out,” stated the MGP expert. And Europe is not a case apart: Spain, in its case, has already brought forward a considerable downgrade in forecasts for this year, a trend that most Eurozone economies will follow. For Alberto Matellán, chief economist at MAPFRE Inversión, the systemic risks in Europe “are several crystal balls put together.” “The median analyst forecast for this year is now 4.5%, a reasonable figure given the current circumstances,” he added.

Such a scenario has made uncertainty in the old continent the central factor on which the rest of the risks are resting. “It is causing damage that is sometimes not easy to measure, but it is clearly indicating lower growth,” explained Alberto Matellán, who also believes that it would be affecting “investment and consumption decisions of companies and families.”

With this, the search for assets that generate profitability in this context of volatility seems more complicated. In this sense, the latest quarterly results of companies could shed some light on investors. “The sample is still small, but the initial data indicate that companies are showing resilience. The important thing is to see how they weather this environment, and for the moment there are encouraging signs,” the MAPFRE Inversión economist acknowledged. However, he stresses that investors should pay more attention to companies' decisions with a long-term view and use active management to “individualize analyses.”