What is the Fed's terminal rate and why is it so important for stock markets?

Redacción Mapfre

In the midst of days marked by downward revisions in activity (from 1.7% to 0.2% for 2022, and from 2.2% to 1.2% for 2023) and unflattering data on inflation (which reached 8.3% in August, lower than July, but worse than analysts' expectations), Morgan Stanley announced that, given the current macroeconomic context, "the revenue forecast for US companies is too high." These data had set off the alarm bells of a possible more aggressive than expected interest rate hike of 100 basis points (bp) by the Federal Reserve, which finally did not happen, given that, according to Ismael García Puente, investment manager and fund selector at MAPFRE Gestión Patrimonial, "such rise would have increased the probability of going into recession and could have given a certain feeling of desperation (the seven previous rises of that magnitude had been in the 70s and 80s)".

Although the Fed finally decided to raise rates by 75 basis points to 3.25%, experts acknowledge that the roadmap hasn’t changed: however much the macroeconomic data worsen, controlling price levels will continue to be the central bank’s number one priority. In fact, since the Jackson Hole symposium, they had already reaffirmed their intention to do whatever is necessary to return to target levels without excessively damaging the economy.

This leads to a kind of vicious circle. And as Alberto Matellán, chief economist at MAPFRE Inversión, points out, "economic activity is already cooling down" which paradoxically, "could make aggressive hikes even more necessary, as the core priority is on getting inflation down before they reboot the economy, so they need to reach their terminal rate as soon as possible. Doing it like this means they’ll have the opportunity to lower rates later, and the impact can be felt sooner."

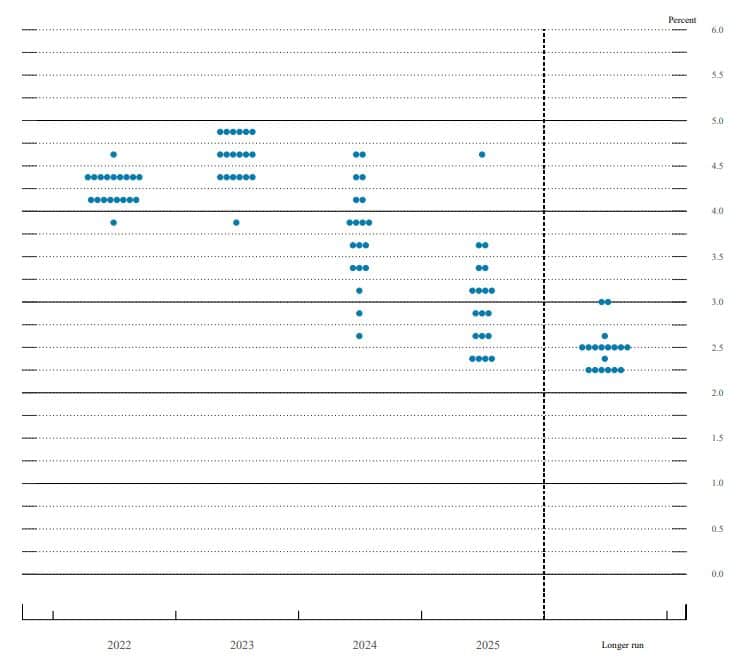

The key is the Fed's terminal rate, i.e., the rate it is willing to go to in order to fight inflation, which is already above 4.5% by the end of 2023. For Matellán, this is the most important indicator for markets, "as it’s the one that shapes longer-term expectations". The big question now is whether the rate will be enough to bring inflation down to around 2% without triggering a major recession. If they finally manage to do what they intend to do, he considers that "we would be in a situation much closer to historical averages than what we’ve seen in the last 10 years". "That would be healthy as long as the unemployment projections are also correct", he adds.

Federal Reserve's Dot Plot

In fact, statistically, "inflation in the US in the middle of next year should come down to around 2-3%", García Puente explains. Its nature, Matellán adds, deriving as it does from domestic demand, makes the problem more serious than it seems, "so the Fed has a greater responsibility". In short, "they have an obligation to keep increasing the price of money, even if the activity data indicate that there is a slowdown in the economy".

But how long does it take for an aggressive rate policy to have an effect on controlling inflation? "Macro manuals and history tell us that a change in monetary policy has an effect around 9-12 months after its implementation", explains Matellán, qualifying that numerous factors may come into play here, thereby impacting the time frame.

In fact, as the expert explains, the inertia of the pandemic (in which the money supply was boosted considerably), together with the nature of inflation (in that in Europe, where price levels are a domestic problem, it arises from an external shock, so that an aggressive monetary policy such as the one currently being adopted faces more problems in halting the inflationary dynamic on the Old Continent than in the United States), means that "it will probably take longer than usual to see the effects of the measures taken by central banks."