The Federal Reserve holds interest rates steady amid an increasingly fragile macroeconomic balance

Redacción Mapfre

Eduardo García Castro, expert economist at Mapfre Economics

The United States Federal Reserve decided to keep interest rates unchanged at what was likely the last meeting chaired by Jerome Powell. This decision was supported by a complex and increasingly narrow balance of risks between economic growth, inflation, and the external environment.

This is a context that does not support a scenario of normalization. Instead, there is a need to buy time during a phase of the cycle in which different macroeconomic components are sending divergent signals, and where the geopolitical situation is narrowing the margin for monetary policy error.

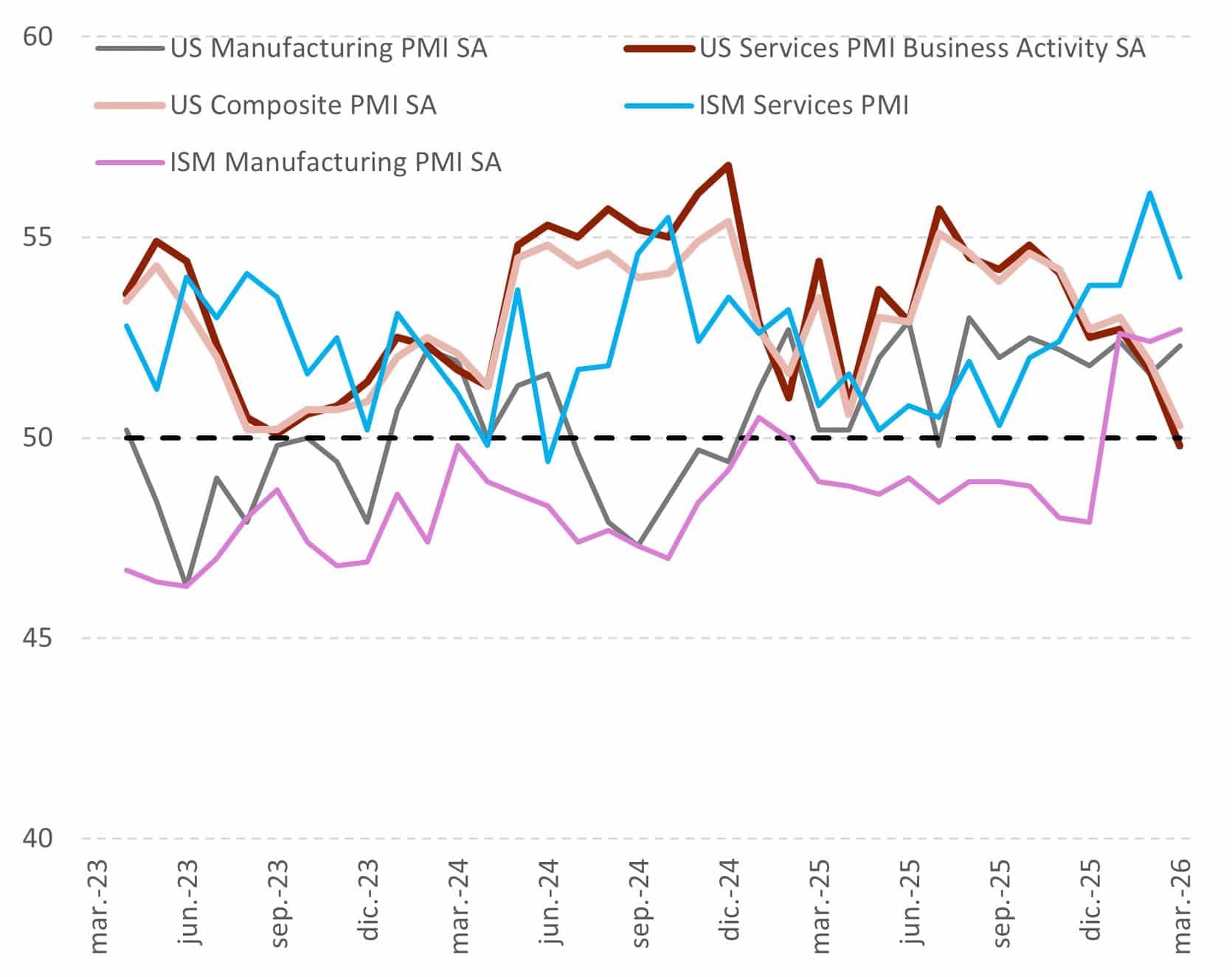

With regard to economic activity, the latest data portrays a U.S. economy that continues to grow, but with a progressive decline in the quality of that growth. The latest leading indicators of activity (ISM and PMI) remain at levels consistent with expansion, although there are increasingly clear signs of moderation in new orders, greater business caution, and a certain loss of momen-tum for employment, especially in manufacturing. Meanwhile, services show that activity levels are being sustained more by inertia and cost passthrough than by a strengthening in final demand (see Chart 1).

This pattern is consistent with the latest consumer and retail sales data, with nominal growth remaining solid. However, that growth is increasingly concentrated in essential and defensive spending, and supported in part by still-relevant fiscal stimulus and elevated prices, rather than by a genuine improvement in real income.

Chart 1. United States: ISM and PMI data

Source: Mapfre Economics (based on Bloomberg data)

In fact, the mixed signals coming from various consumer sentiment surveys (Conference Board and University of Michigan) reflect a situation in which consumers are able to hold up in the short term—supported by employment and fiscal buffers—while confidence about the future continues to decline due to the impact of higher energy costs and geopolitical uncertainty.

In the labor market, the latest data confirms a scenario of economic expansion with lower intensity of job creation (“job-light”). Both the ADP National Employment Report and the latest payroll data continue to show growth, but at a more moderate pace, while other indicators (job vacancies, company surveys, wage growth) point to a less tight labor market, reflecting an unemployment rate that is no longer improving.

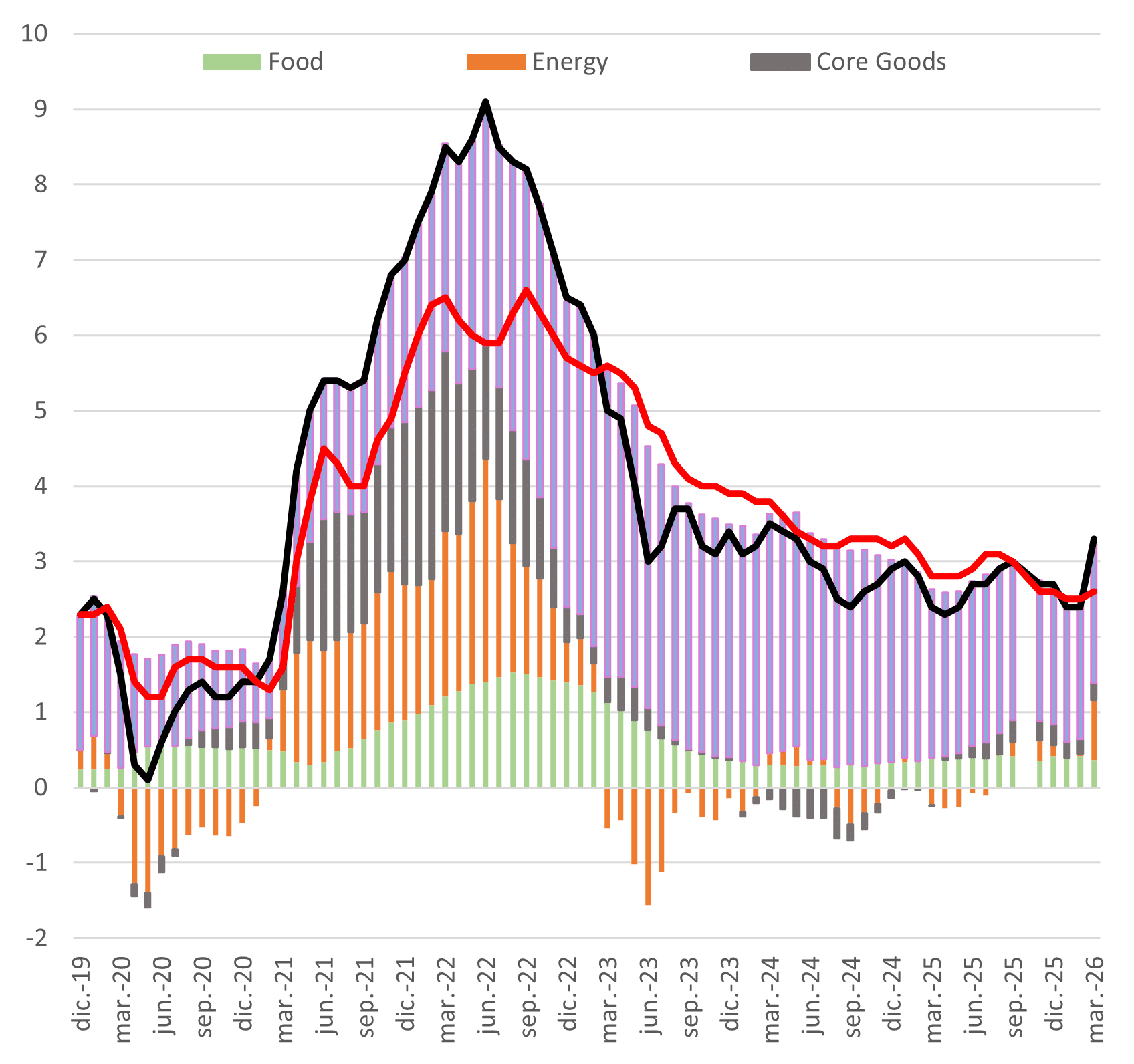

With regard to inflation, March data indicates a rebound to 3.3% YoY, confirming that the disinflation process has lost traction, with some components now operating in a more constrained and uneven environment. While most of this increase has been driven by the energy component and the need for more intensive spending on fuel and logistics, the disinflation process has led to some degree of stabilization in housing and core services (see Chart 2).

This configuration is consistent with the underlying macroeconomic dynamics described above and suggests that, although a gradual slowdown in economic activity can partially ease demand-side pressures, it is not sufficient to offset supply-side pressures. This interpretation therefore supports the idea of a type of inflation that is influenced less by the economic cycle and more by the rising effective cost of energy and the persistence of the shock, which is disrupting the path toward convergence and keeping the balance of risks uncertain.

In addition, all of this is taking place in a geopolitical context that continues to complicate the central scenario, while increasing the likelihood of alternative scenarios, as explained in our report entitled 2026 Economic and Industry Outlook: Second-Quarter Forecast Update. What this means is that the Federal Reserve’s decision reflects a phase of the cycle in which there is no dominant signal, but instead, an uncomfortable coexistence of moderate expansion, persistent inflation, and fiscal buffers that continue to operate, although with diminishing effectiveness. In this context, keeping interest rates unchanged is less a sign of control than of prudence, given the increasingly fragile macroeconomic balance.

Chart 2. United States: inflation by components

Source: Mapfre Economics (based on Bloomberg data)

Institutional succession and the vision of Kevin Warsh

The appointment of a new Chair at the U.S. Federal Reserve is taking place at a time when the context for central bank action has become particularly strained—not so much due to any cumulative policy error, but because the Fed must now operate within a transformed macroeconomic and geopolitical environment. Kevin Warsh will inherit an institution that is facing supply-side inflation, structural geopolitical friction, and an increasingly unstable relationship between economic activity and prices. These are all factors that call into question the traditional effectiveness of monetary policy.

In this regard, Mr. Warsh’s perspective, as reflected in his writings and his recent hearing before the U.S. Senate, is grounded in the central premise that monetary policy cannot serve as a substitute for other economic policies, nor can it correct imbalances of a structural or geopolitical nature. Accordingly, rather than seeking to expand the role of the Federal Reserve, he advocates reaffirming it, with a focus on the fundamental importance of price stability, institutional independence, and strict limits on use of the tools available.

Although the fact that Warsh is the candidate backed by Donald Trump has clearly introduced some tension between this polit-ical appointment and institutional independence, that tension is actually con-sistent with Warsh’s own view of the Federal Reserve. Instead of denying that leadership of the central bank has a political origin, he openly acknowledges this. He stresses the idea that maintaining independence is not about automatically reacting to the priorities of the U.S. president, but rather having the capacity to resist the temptation to use monetary policy to offset fiscal, energy-related, or geopolitical imbalances.

From this perspective, alignment with the government’s political agenda would be less about short-term objectives and more about a shared critique of the central bank’s overreach over the last decade, and this has a direct connection to the type of institution that Warsh will inherit. On one hand, the inflation facing the U.S. economy cannot be corrected automatically through cyclical cooling; on the other, economic growth cannot be sustained un-der the umbrella of temporary fiscal buffers. Therefore, the challenge that Warsh faces is not so much choosing between tightening or easing policy, but managing a framework in which the activity-price trade-off no longer provides a clear signal.

This perspective also explains why Warsh has emphasized the need to prevent the Federal Reserve from becoming implicitly subordinated to short-term stabilization of economic activity or to financing of the cycle, as well as his critical stance toward the current use of inflation indicators as an almost automatic guide for monetary policy. In fact, his approach does not question the goal of price stability, but rather the mismatch between the inflation that is measured and the inflation that monetary policy can actually correct.

In an environment where a significant share of price pressures derives from energy, logistics, housing, and other factors conditioned by geopolitics and physical supply, responding symmetrically with interest rates entails taking on macroeconomic costs without any guarantee of effective disinflation. From this point of view, redefining how inflation is interpreted is not a political concession, but an institutional requirement: better measurements lead to better reactions, while preventing the use of monetary policy as the default tool for absorbing shocks that are not actually under the Fed’s control.

In addition, more disciplined management of tools, such as the balance sheet, would involve an acceptance of short-term costs in exchange for better institutional clarity. Warsh’s focus is therefore on creating a Federal Reserve that is less inclined to off-set all frictions in the system and more centered on preserving the coherence of its institutional framework, recognizing that in the current environment monetary policy cannot, on its own, resolve inherited ten-sions—but it can avoid amplifying them.

Conclusion

The Federal Reserve's decision to keep interest rates unchanged should not be interpreted as a simple pause, but rather as a reflection of a macroeconomic balance where growth, inflation, and geopolitics no longer provide coherent signals for a conventional monetary policy reaction. For the Federal Reserve, neither tightening nor easing guarantees a clear improvement in the activity–price trade-off, and this gives rise to an obligation to priori-tize prudence, consistency, and the preservation of its institutional framework over short-term tactical responses.

It is precisely in this context that Kevin Warsh takes office, with plans to focus on enhancing the clarity of the mandate and preventing the Federal Reserve from taking on tasks that go beyond its actual capabilities. Looking ahead, the main challenge will therefore be to apply this discipline in a politically demanding environment, with more volatile inflation and lower social tolerance for the costs of adjustment. Preserving the central bank’s credibility will require accept-ing that normalization is not automatic, and that monetary policy, while still central, can no longer resolve inherited tensions on its own. In this scenario, the strength of the institutional framework and the clarity of the mandate will likely matter more than the speed of adjustments.