The ECB takes a cautious approach despite inflationary risks

Redacción Mapfre

Eduardo García, expert economist at Mapfre Economics

At its April meeting, the European Central Bank (ECB) kept interest rates unchanged, with the deposit facility at 2.00%, reaffirming a strictly data-dependent approach based on evolving risks. In its communication, the ECB's Governing Council emphasized that inflationary pressures remain exposed to external factors, in an environment of increasing macroeconomic fragility. The ECB stressed the need for caution in light of a balanced risk outlook, characterized by persistent inflation and signs of slowing growth. This assessment moves the economy away from the baseline scenario, without introducing significant changes to balance sheet policy, while reaffirming the central bank’s readiness to act should monetary transmission be impaired.

The downturn in the Eurozone's macroeconomic environment has become increasingly evident in recent weeks, creating a particularly challenging situation for the ECB, given the coexistence of upside inflationary risks and ever more fragile economic growth. This unfavorable balance has gradually fed into interest rate expectations, which now point to a tightening cycle beginning next June.

Regarding activity, signs of economic slowdown have intensified (Eurostat’s preliminary estimate indicates that Eurozone GDP slowed to 0.1% QoQ). Similarly, consumer confidence plummeted, reflecting the cumulative impact of past inflation, rising energy costs, and the loss of real purchasing power. At the same time, other indicators, such as the German IFO and ZEW indexes, once again disappointed, confirming the fragility of the Eurozone’s main industrial driver.

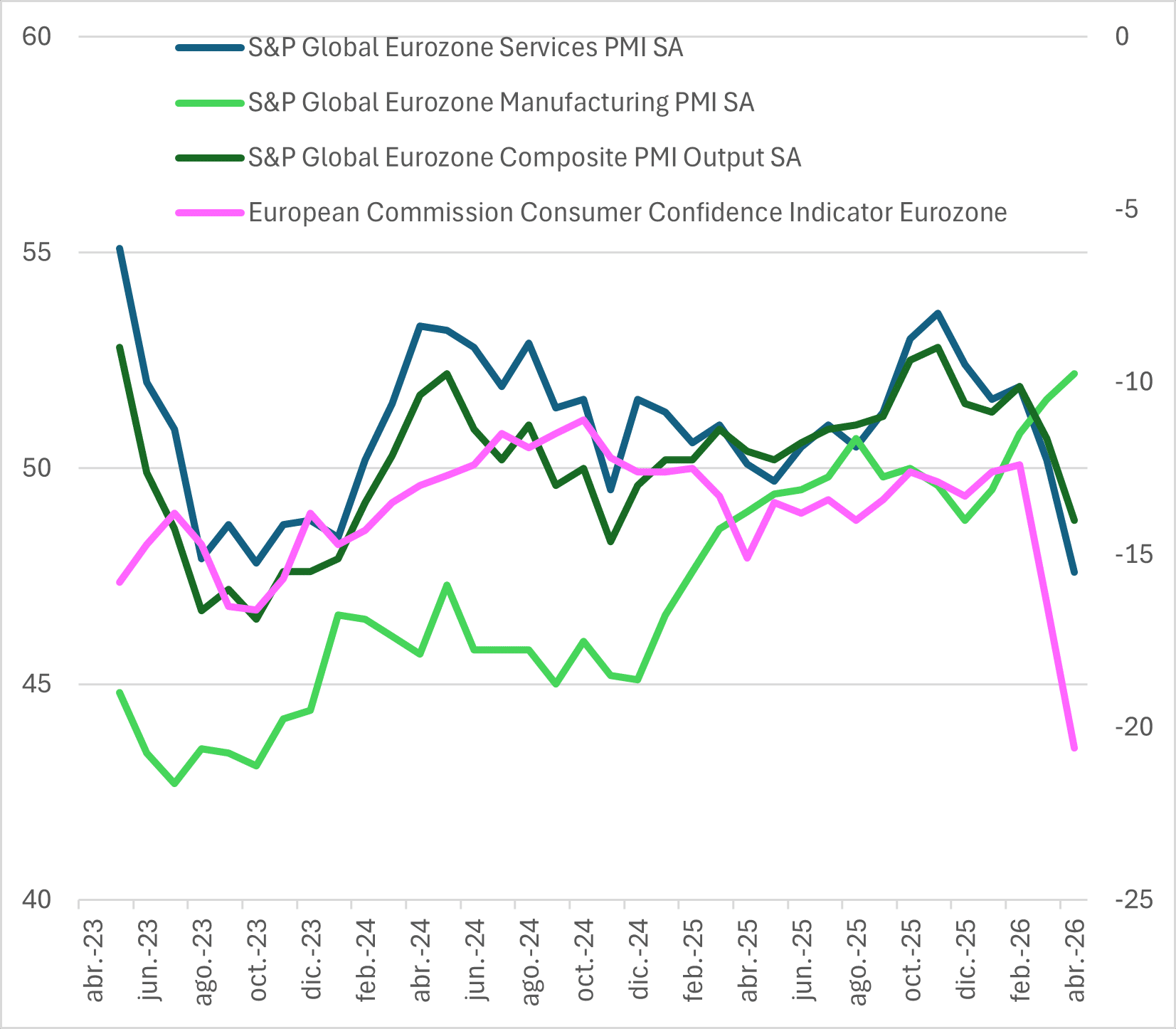

Recent readings of leading activity indicators (PMI) also support this cyclical downturn, with the composite index falling below the expansion threshold in April and signaling the first contraction in private-sector activity in 16 months. The combination of a weakening services sector, an industrial sector unable to recover organically, and increasingly cautious consumers paints a picture in which economic growth is becoming more vulnerable and dependent on exogenous factors (see Chart 1).

Chart 1. Eurozone: PMIs and consumer confidence

Source: Mapfre Economics (based on Bloomberg data)

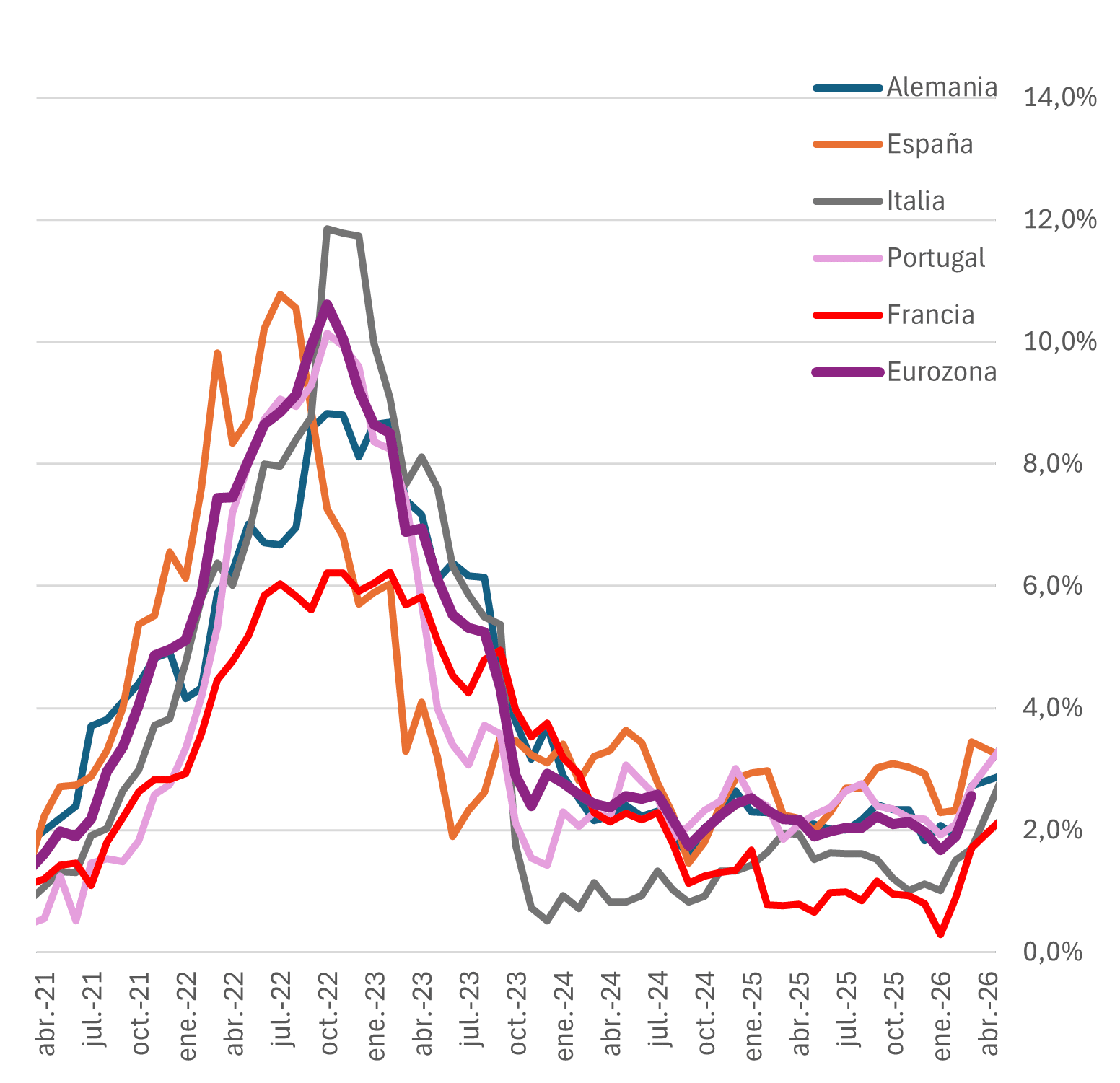

On the inflation side, the latest data reinforces the view of a process driven by persistent supply-side pressures that are relatively insensitive to weakening economic activity (see Chart 2). March CPI for the Eurozone (2.6% YoY) confirmed this trend shift, with significant contributions from energy, transport, and energy-intensive services, while components more closely linked to domestic demand showed only a partial moderation. This pattern was further illustrated by flash CPI data for April at the country level (Germany 2.9% YoY, France 2.2% YoY, Portugal 3.4% YoY, and Spain 3.2% YoY), indicating that price pressures continue to mount.

This is also reflected in short- and medium-term inflation expectations, which have risen in recent ECB surveys. Specifically, the 1-year and 3-year indicators rose from around 2.5% to approximately 4.0% and 3.0%, respectively, while long-term indicators remained relatively stable (2.4%), although at above-target levels.

Overall, these figures reveal a particularly troubling pattern for an economy that is a net energy importer, such as Europe’s, and vulnerable to disruptions in strategic chokepoints like the Strait of Hormuz, where, for now, there is no credible prospect of de-escalation or resolution. In fact, the absence of a credible de-escalation scenario is not merely a backdrop, but one of the main drivers of the current inflationary trend, directly linked to the recent deterioration of the geopolitical energy landscape.

Chart 2. Eurozone: inflation by country

Source: Mapfre Economics (based on Bloomberg data)

In light of recent developments, the Iran conflict seems to have entered a more rigid phase, following the explicit rejection by the Trump administration of Tehran’s latest proposal, along with the decision to maintain and prepare for a prolonged blockade on Iranian energy exports. Moreover, pending further signs of internal tension in Iran, the United States has reiterated that limited military options remain on the table to break the deadlock in negotiations.

This shift has restored a high and persistent risk premium to the oil market, with Brent crude once again reaching 120 dollars per barrel—levels historically associated with periods of open warfare rather than isolated supply disruptions. Therefore, all indications suggest that this is no longer merely a temporary supply interruption, but rather the consolidation of a risk premium associated with a conflict that has entered a more intractable phase, with less room for quick diplomatic solutions.

Conclusion: a change no one wants, but everyone is pricing in

Beyond the specifics of the recent data, the underlying message is that the Eurozone is operating in a structurally more adverse environment, in which traditional adjustment channels function imperfectly. The weakening of economic activity no longer guarantees proportional disinflation, while price pressures are still influenced by external factors beyond the direct control of monetary policy. This decoupling limits the ECB's ability to monitor the cycle and restricts its room for maneuver.

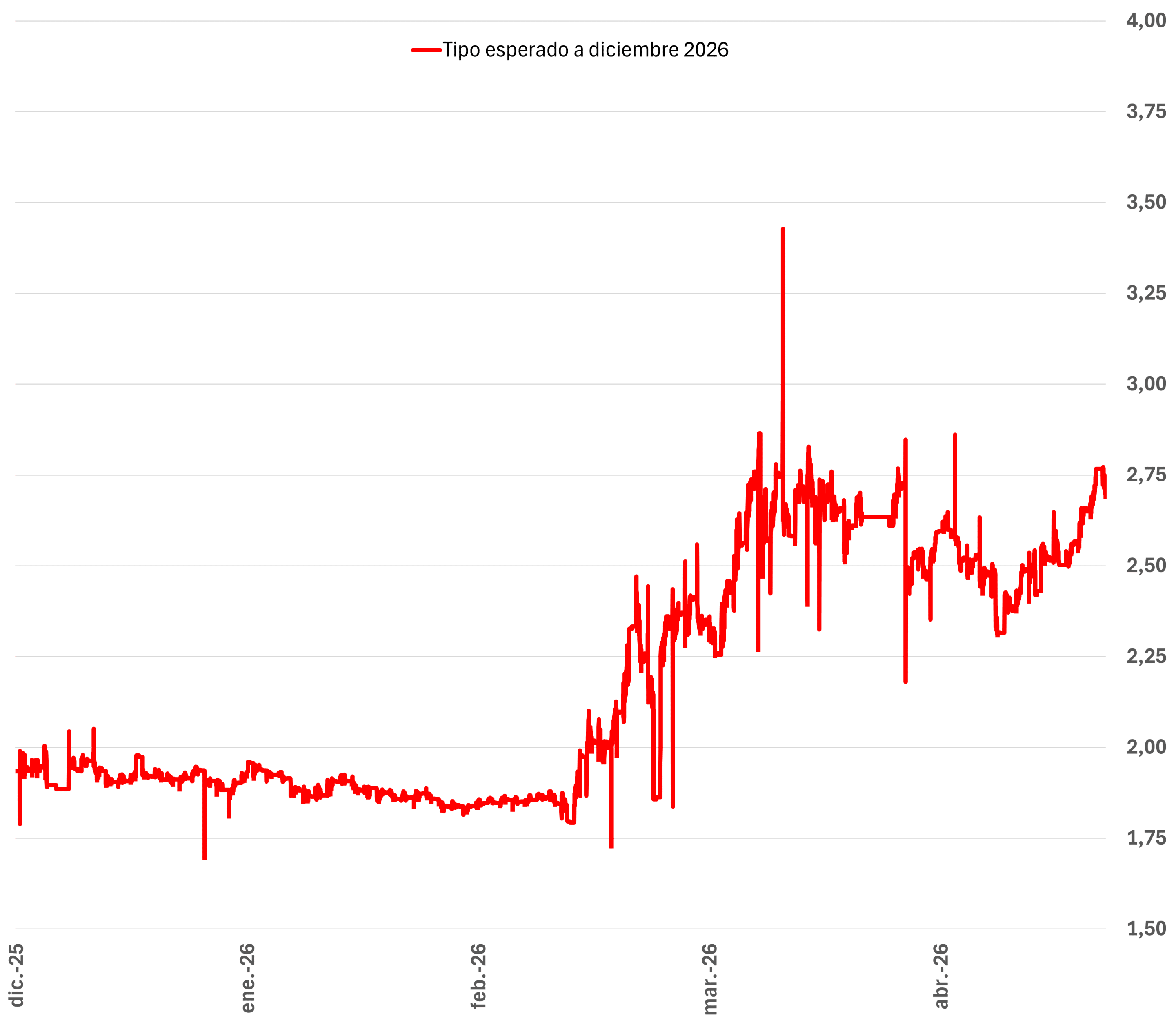

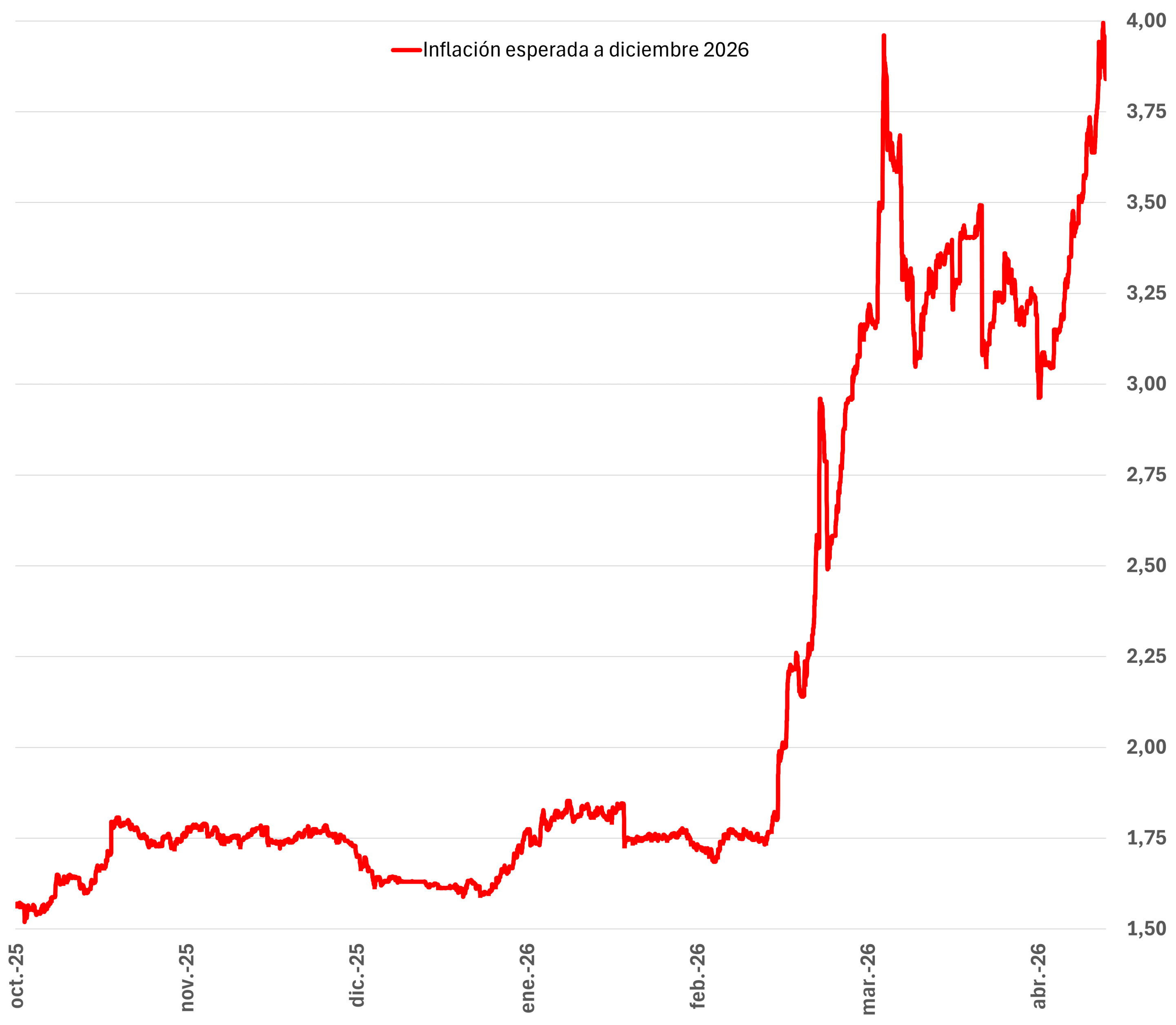

In this context, it is not surprising that the market has begun to price in a tighter monetary policy stance over the one-year horizon (see Charts 3 and 4). Given the rise in inflation expectations, persistent supply-side pressures, and a geopolitical environment that shows no credible signs of normalization, there are no solid arguments to refute this assessment.

Ultimately, the challenge for the ECB is not so much to precisely calibrate the optimal point in the cycle, but to avoid significant monetary policy mistakes in an environment dominated by structural uncertainty, as outlined in our report "2026 Economic and Industry Outlook: Q2 Forecast Update". In this context, the coherence of the institutional framework and the anchoring of expectations carry more weight than the pace of adjustments, and the market’s implicit bias toward a more restrictive policy stance appears to be a reasonable response to the current balance of risks.

Chart 3. Eurozone: interest rate swaps

Source: Mapfre Economics (based on Bloomberg data)

Chart 4. Eurozone: inflation swaps

Source: Mapfre Economics (based on Bloomberg data)