The geopolitical and energy shock seems to be over for equities

Redacción Mapfre

What happened over the past month?

April was a month full of events and news coming from the Persian Gulf, where uncertainty about the end of the conflict remains. The price of a barrel of oil remained high, which continues to increase fears of a scenario of higher inflation and lower growth.

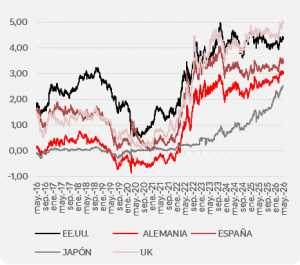

Expectations of higher interest rates weighed on bond yields, which in some countries touched multi-decade highs. This is the case, for example, of the Japanese 10-year bond that surpassed its highest level since 1997, the English bond that reached levels from 2008, or the German bond surpassing the highs of 2011.

.

Gráfico 1: Tipos a 10 años

Even so, it is possible that the peak of inflation fears is now behind us and that concerns are increasingly focused on growth. If that is the case, fixed income still has significant room to perform, as growth forecasts have been repeatedly revised downward, creating a more favorable environment for government bonds.

We also saw strong movements in corporate bonds. The announcement of a temporary ceasefire at the beginning of the month served to sharply reduce credit spreads. In fact, by the end of April, spreads on higher-rated bonds had returned to the levels at which they had started the year. In the high-yield segment, the risk appetite that prevailed during April also supported this type of bond. However, concerns about the health of private debt, together with a return of activity in the primary markets following a March with limited issuance, prevented spreads from approaching their historical lows.

The geopolitical and energy shock appears to be behind equity markets. Global stock markets rose by nearly 10% in April, driven mainly by U.S. indices, which reached record highs. This marked the best month for the S&P 500 since November 2020 (+10.5%), following the announcement of a coronavirus vaccine.

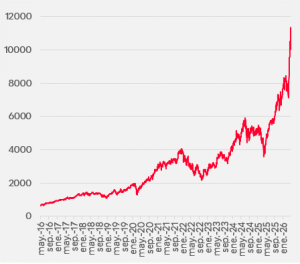

The stellar performance of the U.S. stock market was supported by two factors: on the one hand, improving corporate earnings expectations, driven by the United States’ stronger position to weather the energy shock; and on the other, a renewed strong appetite for companies related to artificial intelligence. More specifically, this included firms involved in the manufacturing of semiconductors—key components for this emerging technology—as reflected in the fact that the main index for this sector, the Philadelphia Semiconductor Index, recorded its best month since February 2000, rising 38%.

.

Gráfico 2: Índice Semiconductores

Strong demand for these technological components also benefited other stock markets, such as those in Asia, where a handful of companies account for a large share of semiconductor production. The MSCI Asia Pacific index rose by 13%, as the Korean stock market climbed more than 30%, supported by companies such as Samsung and SK Hynix (+33% and +60.55%, respectively). European stock markets also had a positive month but lagged behind the returns seen in other regions.

Despite the strong performance of U.S. equities, the euro appreciated by 1.54% against the U.S. dollar, while gold declined to $4,600 per ounce and has still not performed as strongly as expected.

What's our take?

Despite the truce to begin negotiations announced in early April, which could reduce uncertainty in the region, the conflict in the Middle East continues. The energy shock is beginning to affect production and supply chains, with a potential impact on demand through rationing and physical restrictions.

Neither side is interested in prolonging the conflict, but both the United States and Iran believe that time is on their side. Iran believes that the United States will eventually yield to its demands due to the negative effect the conflict has on the financial markets, the proximity of mid-term elections, and costly weapons to replenish. On the U.S. side, President Trump's statements abound in which he claims that the United States is winning the war since the Iranian regime is completely decapitated and the lack of oil revenues due to the strait blockade will force the country to seek a quick solution. In the short term, it is possible that we will see escalating tensions in the area since both countries could try to obtain a better position from which to negotiate.

With the Strait of Hormuz closed, one wonders how long the oil reserves will hold out. It is estimated that countries are holding around 1.2 billion barrels in storage, which, combined with 600 million barrels in private reserves, brings the total to 1.8 billion barrels. Taking into account the oil being released by Gulf producer countries through pipelines and a global daily demand of around 100 million barrels, these reserves would be sufficient to guarantee supply until mid-July. From then on, demand destruction would be more palpable with its corresponding impact on growth.

As the duration of the conflict can no longer be considered short, the continued closure of the Strait of Hormuz and damage to energy infrastructure, our base scenario has changed, as we already noted last month. The global economy is now operating in a different environment, where inflation will be more persistent and the risks of stagflation have increased (especially in Europe and Asia). In this new scenario, we have revised inflation forecasts upward to a greater extent than we have revised growth forecasts downward (see macroeconomic forecast table), as we are still far from the most adverse scenario.

With the conflict now approaching its third month, the macroeconomic data released so far shows some divergence: indicators based on sentiment surveys (PMIs, consumer confidence, leading indicators) point to a greater deterioration than is currently reflected in lagging data such as GDP, the labor market, or inflation itself. However, the first negative surprise came from growth in the Eurozone, which increased by just one tenth in the first quarter of the year, compared with the expected 0.2% and the previous quarter. With only one of the three months in the quarter affected by the war in Iran, and given the recently published sentiment readings, we could see a contraction in GDP in the second quarter.

Tightening credit conditions are also beginning to have an impact. According to the latest ECB survey, European banks have tightened lending conditions at the same time that demand for loans has fallen to its lowest level since the end of 2023. This shift in banks’ perception of risk gives the ECB some time to assess the real impact on the Eurozone and adjust its monetary policy, as weaker credit flows tend to support the anchoring of inflation expectations. The ECB kept interest rates unchanged at its latest meeting, where C. Lagarde acknowledged that the economy was moving away from the baseline scenario updated in March (in line with our view). She also suggested that June is likely to be the month chosen for a rate hike in the Eurozone, as already priced in by market consensus, with a further increase probably in September.

In the case of the United States, there were also no changes in interest rates, as the main shift is expected next month with the new Federal Reserve Chair taking office. Kevin Warsh arrives with the challenge of strengthening the Fed’s independence and preventing the Federal Reserve from taking on responsibilities beyond its mandate. All of this comes in a demanding and geopolitically turbulent environment, where markets are hoping for rate cuts, but for now none are priced in.

Surprisingly, despite the strong revaluation in April, U.S. equity markets are currently trading at more attractive multiples than at the beginning of the year. The forward price-to-earnings (P/E) ratio stands at around 20x, compared with 23x in January 2026. This is because earnings are continuing to grow at a much faster pace than prices. We are on track to close the quarter with year-to-date earnings growth of 25%, whereas just a few months ago the market was only expecting around 11%.

The return of American exceptionalism is a reality, as is the market’s focus on the investments needed to deploy artificial intelligence tools. Major technology companies have invested more than $150 billion during the first quarter of the year and have committed over $1 trillion for the coming years. It is now the market's task to foresee which of these companies will translate these investments into greater profits, since the counterpart of this CAPEX is increasingly lower free cash flows for shareholders.

Risk appetite is also being fueled by an expected wave of major IPOs in the coming months, with an estimated combined market capitalization of around $2 trillion. Given their future size and the change in rules announced by Nasdaq, these companies could have a very significant weighting in indices (even if their free float is low), which in turn is likely to generate strong demand from passive fund managers.

What are we doing?

We have not modified our asset allocation despite the strong performance of equities. It is difficult to position against such a strong trend, which is why we prefer to maintain equity exposure in our portfolios and tilt relatively toward U.S. equities. In fixed income, we have slightly increased our allocation to corporate bonds, which remains our highest-conviction asset class, and we continue to keep duration slightly above our benchmark indices. In terms of positioning, we have increased our exposure to inflation-linked bonds in Spain, with the aim of generating returns if inflation remains elevated.

Chart of the month

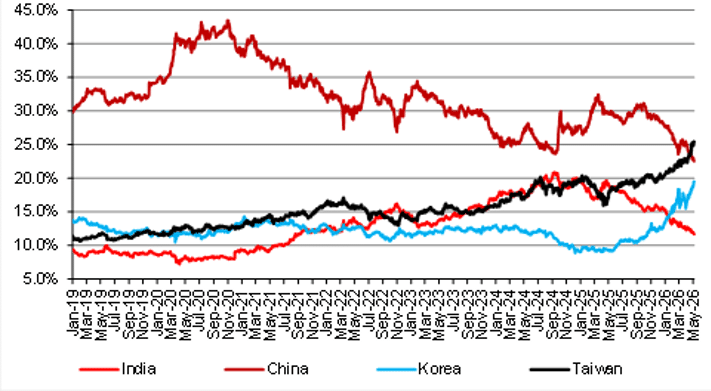

Change in stock market leadership

Taiwan is set to become the country with the largest weight in the MSCI Emerging Markets and MSCI Asia ex-Japan indices, replacing China, whose weighting has declined from more than 40% to around 25%.

Taiwan’s strong exposure to semiconductors, led by industry leader TSMC, has driven this sharp rise in its equity market. If this trend continues, the next market likely to see a significant increase in index representation would be South Korea, which also has substantial exposure to semiconductor manufacturing companies.

Thus, the concentration in the technology sector is not only a clear reality in the United States but is also becoming a global phenomenon. This increasing weight will also attract greater attention from global investors (and passive fund managers). The downside of this rising concentration is that, if market conditions become less favorable, the resulting declines could also be more abrupt.

Another interesting point to highlight is China’s displacement as the largest stock market within emerging markets, despite having a higher total market capitalization than Taiwan. However, a lower presence of technology companies and the index providers’ calculation methodology have led to this overtaking.

Peso en el MSCI Emerging Index

Fuente: MSCI, Nomura